HECO in the Spotlight – Part 2

Struck between Shareholder Priorities, Customer Priorities, and States Mandates – HECO is adrift…

Investor-owned utilities (IOUs), as is the case with HECO, are the old-school, for-profit, regulated-monopoly utilities, with a captive customer base and profits guaranteed by law. Yet, Hawaii’s 2045 clean energy (RPS) mandate requires HECO to institute operating reforms that must, first and foremost, address needed changes without endangering the stability or economic efficiency of Hawaii’s electricity system.

IOUs like HECO, were also the driving force behind their successful drive to slow-to-a-crawl the nationwide expansion of residential and business installed rooftop solar and their independent clean power contributions to the grid. A strange paradox for utilities like HECO who viewed this subset of utility customers with solar installed as competitors. (for more on this see “HECO in the Spotlight – Part 1”)

Hawaii’s island-based electricity systems are most likely too small to host competing same-island utilities, but not the robust expansion of distributed clean energy options in the form of residential and commercial rooftop solar and storage.

Last week Bloomberg reported that activist investor ValueAct Capital Management (a San Francisco based hedge fund and investor in HECO, is urging that the company to look outside for a replacement and successor to HECO’s current Chief Executive Officer Constance Lau, and one that will lead the utility on path that accelerates its renewable energy goals. Something the utility has failed to do, and 100% statewide renewable energy objective, and the clock is running down out fast… for Hawaii and HECO.

“The company (HECO) is at an inflection point where management can be driven either by more of the same inertia or, alternatively, by innovative, forward-looking thinking and action,” ValueAct Chief Executive Officer Jeff Ubben said in a letter to the company dated Nov. 11. “I firmly believe the best candidate for this crucial leadership role will be found outside of the company. The problem starts at the top, Hawaiian Electric Industries executives and its board leadership have been richly rewarded for lackluster performance.” Ubben said.

Ubben said at the time that ValueAct planned to push the utility to accelerate its use of renewable energy, among other changes. He said in the letter this month that he was encouraged by the utility adding three new directors to its board in February. But was disappointed that two of them, renewable energy veterans Mary Powell and Celeste Connors, weren’t assigned to any board committees, and he believes the entrenched leadership style and culture at Hawaiian Electric holds the company and Hawaii back from realizing its full potential.

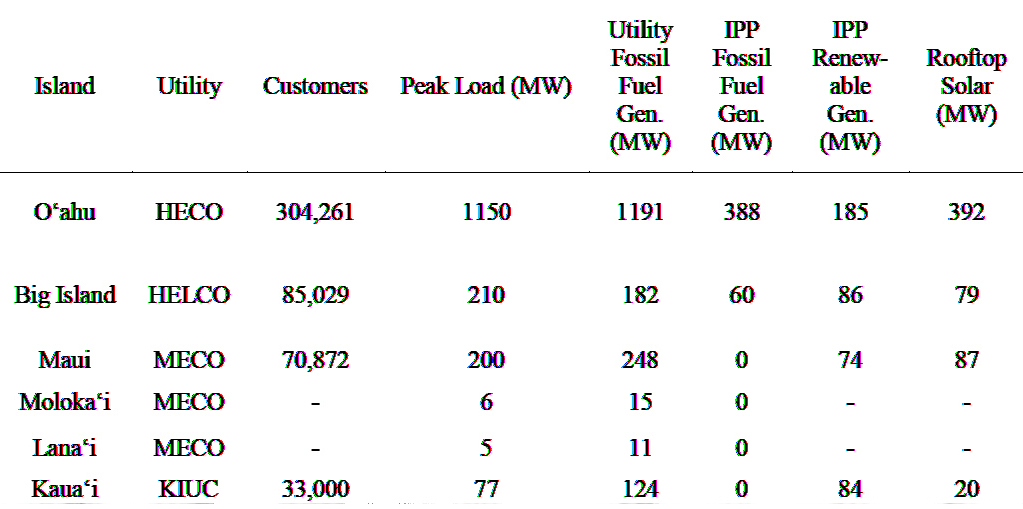

ValueAct correctly observed that HECO remains far too reliant on imported oil, which is used to produce 63% of its electricity, leading to higher rates for its customers. Also a far distance from reaching its 100% renewable energy mandate in the 20 plus years.

HECO and other investor-owned and regulated electric utilities continue to go back to well, a deep one, managed by Public Utility Commissions across the country. PUC’s generally engage in rate-making (raising the cost of power to ratepayers) in a process that requires utilities to:

1) estimate how much power their customers will need;

2) estimate the investments they’ll need to make in power plants, fuel, transmission lines, etc. in order to meet that demand;

3) estimate what rate they need to charge customers to cover those investments and offer a reasonable “rate of return” to their investors;

4) make a “rate case” justifying the rate increase; and

5) if the PUC signs off, the Utility is free to charge is customers the new rate increase, and until the next time when they make their case for another rate increase.

Hawaiian residents have paid 280% more for electricity per kilowatt hour than the U.S. average over the past 10 years. HECO recently filed with Hawaii’s PUC regulators for another rate increase. It is more than the retail cost of energy that brothers many of Hawaii’s residents footing the bill for HECO’s slow-motion dance to clean energy, it’s what HECO does with all those ratepayers dollars (pollute or protect Hawaii’s environment) that also matters to the state’s future and to all Hawaii stakeholders.

The real question is just what form should HECO’s electrical system take to best meet the challenges of the state Renewal Portfolio Standards and it’s 100% renewable energy deadline by 2045. If recent history is any indicator, the utility will be late and short on their regulatory commitment to Hawaii’s residents, and at a cost to ratepayer that is higher than necessary (e.g. HELCO – Hu Honua power purchase agreement).

“The company is at an inflection point where management can be driven either by more of the same inertia or, alternatively, by innovative, forward-looking thinking and action,” ValueAct Chief Executive Officer Jeff Ubben said in a letter to the company dated Nov. 11. “I firmly believe the best candidate for this crucial leadership role will be found outside of the company. The problem starts at the top, Hawaiian Electric Industries executives and its board leadership have been richly rewarded for lackluster performance.” Ubben said.

HECO and other investor-owned and regulated electric utilities continue to go back to well, a deep one comprised of ratepayers and managed by PUC’s across the country.

Like any business, utilities must justify their product cost to their target customers, and in the case of regulated utilities like HECO they also engage in rate-making processes before their governing public utility commission (PUC) that includes:

1) estimating how much power their customers will need;

2) estimating the investments they’ll need to make in power plants, fuel, transmission lines, etc. in order to meet that demand;

3) estimating what rate they need to charge customers to cover those investments and offer a reasonable “rate of return” to their investors;

4) then, they go to the state public utility commission (PUC) to make a “rate case” justifying the rate;

5) if the PUC signs off, the Utility is free to charge is customers the new rate increase, and until the next time when they make their case for another rate increase.

Hawaiian residents have paid 280% more for electricity per kilowatt hour than the U.S. average over the past 10 years. HECO recently filed with Hawaii’s PUC regulators for another rate increase.

It is more than the rising cost of energy that concerns Hawaii’s residents, it’s footing the bill for HECO’s slow-motion dance to clean energy while subsidizing high imported fossil fuel costs to power HECO’s grid. And the there is the question of what HECO does with all those ratepayers dollars; pollute or protect Hawaii’s environment. That too matters to the state’s future and to all Hawaii stakeholders.

Another possibility, and one seriously considered during the height of the NextEra takeover controversy, is the transformation of HECO from a privately owned utility to a municipality or electricity cooperative, possible one that is better aligned with the state’s clean energy objectives and that of the public interest – an option with the potential to work well for Hawaii (e.g. Kauai’s KIUC). If Maui’s electric utility cooperative and its advance state of renewable energy deployment and utility scale battery storage is any indication, then the transformation of HECO from a privately owned utility to a municipality or electricity cooperative appears better aligned with the state’s clean energy objectives and that of the public interest.

In decision time line more analogous to wrap speed, as compared to HECO horse and buggy decision cycles, Kissimmee Utility Authority (KUA) engaged in a groundbreaking event in November for the “Florida Municipal Solar Project”, a large-scale solar energy project that will enable KUA to provide renewable energy to its customers beginning next summer– a six month timeline from groundbreaking to clean power being delivered to Florida residents.

The Project is one of the largest municipally-backed solar projects in the United States, and is a joint effort between KUA and 11 other Florida municipal electric utilities, the Florida Municipal Power Agency (FMPA) and Florida Renewable Partners, LLC. A total of 900,000 solar panels will be installed at two sites in Osceola County and at one site in Orange County — enough solar panels to fill 900 football fields and with a total generating capability will be 223.5 megawatts of zero-emissions solar energy; enough to power 45,000 typical Florida homes.

The question remains… what form should HECO’s electrical system take to best meet Hawaii’s Renewal Portfolio Standards and 100% renewable energy deadline by 2045. If recent history is any indicator, the utility will be late, and will be short on their regulatory commitment to Hawaii’s residents, and likely at a cost to ratepayers that is far greater than necessary.

Headline Update

“Scott Seu, a senior vice president at Hawaiian Electric Company, will succeed Alan Oshima as president and chief executive officer of the company effective in the first quarter of 2020.” Hawaiian Electric Press Release, December 10, 2019.

…In December 2006 Scott Seu testified as a HECO witness before the Public Utilities Commission:

“Q. Do they believe that climate change is occurring? A. I — I don’t know off the top of my head…”

By Seu’s answer in 2006, you’d think his answer was from 1986, not 2006. Seu may be good for shareholder interests, until those interests have opportunity costs for both HEI and the state of Hawaii in the form of higher energy costs and lost opportunities to transform the company into a clean energy provider instead of remaining a fossil fuel retailer of dirty energy between now and 2045.

William Giese, executive director of the Hawaiian Solar Energy Association, said he hopes Seu can help HECO embrace changes better than it has so far.

“My quick reaction is that Scott is a nice guy, and it seems like he’s competent,” Giese said. “But he’s also been at HECO for a long time, so hopefully he can shake the chains of institutional bias that have been at HECO for a while.”

Leave a Reply

Join the Community discussion now - your email address will not be published, remains secure and confidential. Mahalo.